Uniswap Liquidity Mining Retro

Background

On July 14, Gauntlet announced a liquidity mining program on Uniswap. Over the next 2 weeks, roughly 49k UNI was distributed to liquidity providers across 8 Uniswap V3 pools on Ethereum mainnet. Now that we have seen a few weeks of post-incentive data, we can review the results of this round of spending to see where it was most effective.

Our program aimed to test whether our initial methodology could create self-sustaining growth via liquidity mining. By incentivizing liquidity in the targeted pools, we aimed to attract a greater market share of volume and sustain this greater share after the end of the program. With this goal in mind, we especially targeted pairs with high market-wide trading volume, but a low market share of volume on Uniswap v3. The pool selection methodology was based on a simulation of volume and liquidity in the pools. In this initial model, we made 2 simplifying assumptions, which we aimed to test and refine in later iterations:

- LPs are perfectly elastic to incentives and will continue to add liquidity until the pool APY returns to its pre-incentive level

- Volume market share follows liquidity market share, so pools that increase in liquidity will attract volume from other exchanges proportionately

We chose this starting point based on our previous analysis of liquidity mining on Optimism, where we observed similar behavior in the pools that responded well to incentives. Since there are many unknown factors that could affect either of these assumptions, we aimed to validate and adjust them through a series of small incentive programs.

Summary Results

In this first program, we focused mainly on growing established pools with relatively low market share and bootstrapping pools with minimal existing activity. If our hypotheses were confirmed, liquidity mining should be effective at generating some long-term sustained benefits for both of these types of pools. The pools targeted were of broadly 2 types:

- 3 larger pools with >$1M TVL and >$1M average daily volume initially

- LST pool (wstETH/ETH 0.01%)

- Stablecoin pool (DAI/USDT 0.01%)

- Volatile pool (LDO/ETH 0.3%)

- 5 smaller volatile pools with lower initial volume and TVL

- SYN/ETH 0.3 %

- FXS/ETH 0.3 %

- PENDLE/ETH 0.3 %

- ILV/ETH 0.3 %

- VEGA/ETH 0.3 %

The table shows the initial parameters and estimated impact for each of the pools. The impact metrics are the change in TVL, the change in volume relative to overall DEX volume for the assets, and an estimate of discounted cash flow from increased fees over the next year assuming the protocol fee switch were to be turned on (the future cash flow of the Uniswap Objective function).

While we do not project a positive ROI for this program over the next year on a discounted cash flow basis, we were able to draw many learnings that will make future iterations of liquidity mining programs more likely to be successful. As a result of this program, we have gathered valuable insights into the behavior of LPs and traders. In particular, we derived 2 significant insights that can help refine our original modeling assumptions:

- LPs were not always sensitive to incentives and sometimes failed to respond. We observed LPs in some pools seemed to be unaware of the program entirely and did not claim their rewards.

- Volume market share was not always directly linked to liquidity over the time frame of our program. Some pools that gain a lot of liquidity failed to attract a significant share of new volume, either due to a lagging effect or other yet unknown reasons.

Applying these insights, we will be able to create improved iterations of our incentive model for future programs. Through better predictive models of LP behavior in response to incentives and trader behavior in response to liquidity, we will be able to more accurately adjust incentive spending and pool selections in order to increase the likelihood of a positive ROI. This work is already underway and will use the data generated from this initial program.

In the rest of this retro, we will go through some more detailed analyses of user behavior in each pool we incentivized and conclude with our planned next steps for our more robust modeling effort.

Large Pools

wstETH / ETH

The wstETH / ETH 0.01% pool was the most heavily incentivized, receiving about half of the total rewards distribution. In the figures below, the first vertical red line shows the start of the incentive program (July 14th) and the second vertical red line shows the end of the incentive program (July 28th). During the program, the pool saw huge growth in liquidity and TVL. In particular, the liquidity at the current tick (which represents the virtual reserves in the pool based on the current price and the price ranges at which LPs allocated liquidity) increased by about 100% from roughly $10m to $20m, theoretically enabling much more trading depth.

Unfortunately, it would seem that volume did not respond strongly to this increase in liquidity, going against our prior expectations. Despite a doubling of in-range liquidity, there was no statistically significant increase in volume during the incentives period (there was an increase after the incentives program ended, but this is likely due to the Curve hack which occurred directly afterward). This lack of volume response prevented liquidity bootstrapping from taking effect and reduced the long-term impact on this pool.

We will be using this data to further explore volume attribution and dynamics to better understand at what threshold of TVL we would expect traders to react. This experiment provides valuable insights into this question which we will be working to answer through a volume simulation currently under development.

LDO / ETH

The LDO / ETH 0.3% pool was the largest pool incentivized, starting with over $15M of initial TVL. Our incentive program does not appear to have had a significant effect on volume or liquidity in this pool. Volume market share has been higher since the end of the program, but this may also be due to unrelated issues (such as the Curve exploit) with competing pools.

Also, as we will discuss later in this retro, almost no LPs in this pool have claimed their earned rewards. The small incentive amount relative to the size of the pool and lack of visible response leads us to conclude that the impact in this pool was not material, possibly due to a lack of awareness or insufficient reward amounts.

This pool faced a different issue than the wstETH pool – while the wstETH pool saw little reaction to LPs adding liquidity, the LDO pool saw little reaction from LPs in the first place. It is currently unclear if this is due to insufficient marketing, too low of an incentive, or other extraneous factors. However, we will be using this data to train and test future liquidity models in order to better understand LP behavior in response to incentives.

DAI / USDT

The DAI / USDT 0.01% pool was the only stablecoin pool we targeted. While the incentive program seems to have had a strong impact on TVL (going from $3m to over $6m), there was only a small impact on trading volumes. In fact, the volume market share for this pool has declined fairly substantially from the pre-incentive level, though this may be due to unrelated factors around the competing Curve 3pool.

We will be using this data to calibrate future iterations of our liquidity and volume modeling in order to better understand the amount of liquidity that is necessary in order to influence trader behavior to re-route potential orders.

Small Pools

We also incentivized 5 smaller pools with the goal of bootstrapping significant usage where minimal activity existed previously. Some of these pools saw significant gains in volume and liquidity, but others had an insignificant impact.

FXS / ETH

The FXS / ETH pool was the most established of the small pools we targeted, but had been in a gradual decline for some time prior. We saw a modest increase in liquidity going from $275k to $325k with a similarly modest increase in volume going from ~10% market share to ~20% market share during the incentives program. We have seen volume market share has been slightly higher so far in the post-incentive period, and while TVL has resumed its decline and is now below the starting value, the liquidity is more efficiently concentrated around the current price. This is an example of a small success where volume market share was maintained at a slightly higher equilibrium however both TVL and volume did not react as strongly as we would have expected based on initial assumptions.

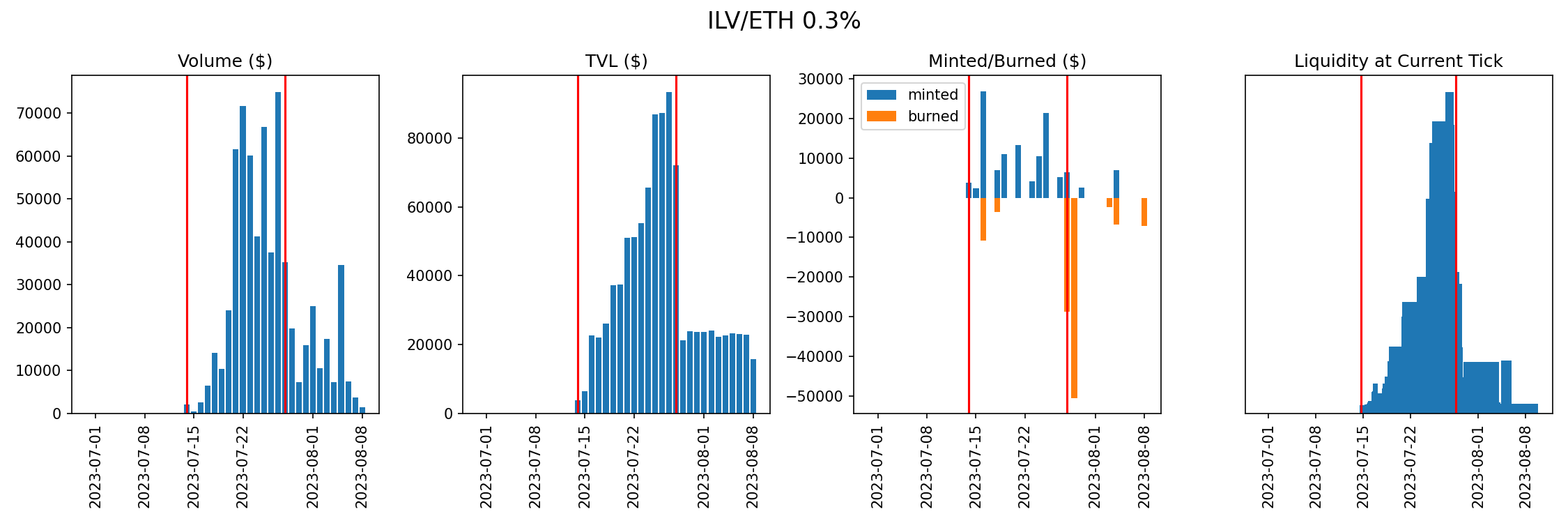

SYN / ETH & ILV / ETH

The SYN / ETH and ILV / ETH pools had effectively zero usage prior to our incentive program and attained sustained liquidity and volume after the program. While the liquidity and volume are lower than they were at the peak, they are much higher than they were before incentives were introduced. This confirms the observation from our Optimism analysis that liquidity mining can be useful for bootstrapping unused pools off the ground. While we were successful in growing these pools through this program, the incentives were not enough to topple competing pools on other DEXs. It is possible that a longer or larger incentive program may have helped more firmly establish these pools, which is another area we are reviewing for further refinement.

PENDLE / ETH

The PENDLE / ETH pool was notable due to the high volatility of PENDLE shortly after the incentives began. We noted that few users seemed to react to the program, which we attributed to the activity being driven mainly by price action and the high risk of impermanent loss. Though the volume market share of this pool has been quite strong recently, we cannot conclusively say whether this was related to our incentives program or other factors entirely. We noted that incentivizing assets during high volatility periods can affect user responses and make it difficult to assess impact.

VEGA / ETH

The VEGA / ETH pool was the least incentivized of all pools, receiving only ~280 UNI of total rewards. We did not see significant effects from this spending, and it may have been too small for prospective LPs to consider adding liquidity. We note that future programs could consider some threshold for incentive size to help mitigate this issue.

Claim Rate Analysis

Due to the relatively small program overall, some users may not be aware that they have earned rewards. We saw significant variation in claim rates across pools, which may be a confounding factor in assessing impact. Unclaimed rewards mean that LPs were not incentivized to respond to the program as intended, which would negatively affect program efficiency. More analysis is needed to understand how LP awareness may have affected efficiency and potential strategies to address this in the future.

In the large pools, we noted a huge difference in claim rate between the wstETH pool where the majority of LPs claimed rewards, and the LDO pool where almost no rewards were claimed. This likely explains why the LDO / ETH pool saw minimal impact, as discussed earlier. In the figure below, each bar represents an LP in the pool, with the height of the bar showing the total amount of UNI they earned through this program. The orange bars show UNI claimed within a week of the program ending, and the blue bars show UNI that has been earned but not yet claimed.

The claims data was also notable for the DAI / USDT 0.01% pool, where one large LP was an outlier in claiming their rewards. We conclude that apart from this user, most stablecoin LPs were likely unaware of the program or considered it immaterial. This may also explain why the impact on this pool did not seem to persist.

In contrast, the SYN / ETH and ILV / ETH pools saw a fairly consistently high claim rate across all LPs. Since these pools started out with near-zero TVL, this may suggest that most of the LPs in these pools were well-informed and added liquidity primarily due to being directly aware of the program.

The remaining small pools saw a mix of LPs who claimed and did not claim. More granular analysis of claim patterns may help us better understand LP behavior and design more efficient programs in the future.

Next Steps

This liquidity mining experiment was our first attempt at a data-driven approach to designing incentives that maximize protocol growth with a limited budget. To do so, we made some simplifying assumptions about how LPs and traders operate. While this round of incentives did not generate a net positive hypothetical cash flow (our proposed method for ROI), it was successful in invalidating some of our original assumptions, and it provided good learnings for future LM programs. In particular, we managed to gain the following key takeaways:

- LM incentives are useful for helping dead pools gain TVL and volume (SYN, ILV)

- For more established pools with many existing LPs, it can be much harder to have an impact as there appears to be less liquidity elasticity with respect to rewards (LDO)

- Volume is not necessarily elastic to liquidity, which can hamper the flywheel effect we seek in a liquidity mining program (DAI/USDT, wstETH)

- LPs would benefit from increased awareness of the program and methods of claiming, as we can see that many LPs were not aware of the rewards they earned: this could include a more active publicity campaign, more advertising from UF and Gauntlet, etc.

- The commanding market share Uniswap has on Ethereum makes it harder to make LM have positive ROI, because there are diminishing returns to incentivizing an already large pool to get even larger.

We will be using the learnings in this initial experiment to build a simulation model to better understand and predict the relation between incentives, liquidity, and volume. It is our belief that with a better-calibrated model, we will be able to run higher ROI programs in the future, after better understanding the dynamics of LPs and Traders.